By Marcello Estevão, Global Director, Macroeconomics, Trade, and Investment Global Practice – World Bank

Global warming is real and climate disasters are believed to be occurring with higher frequency. The heightened risks and sizeable setbacks can move economies onto trajectories characterized by lower growth rates, greater financial and fiscal instability, and even poverty traps. This is especially true for more vulnerable developing countries. Our recent report, Fiscal Policies for a Low-Carbon Economy, suggests how a mix of carbon taxation and green bonds can address climate-related risks, improve economic recovery plans, and facilitate a transition to a low-carbon economy.

Research on climate economics finds that green bonds can accelerate a low-carbon transition, may have a positive impact on aggregate output and employment, help to advance renewable energy technology, address better the issue of fair transition, and be a stabilizing force on the financial market compared to conventional, in particular fossil fuel-based, assets. Our research confirms these findings.

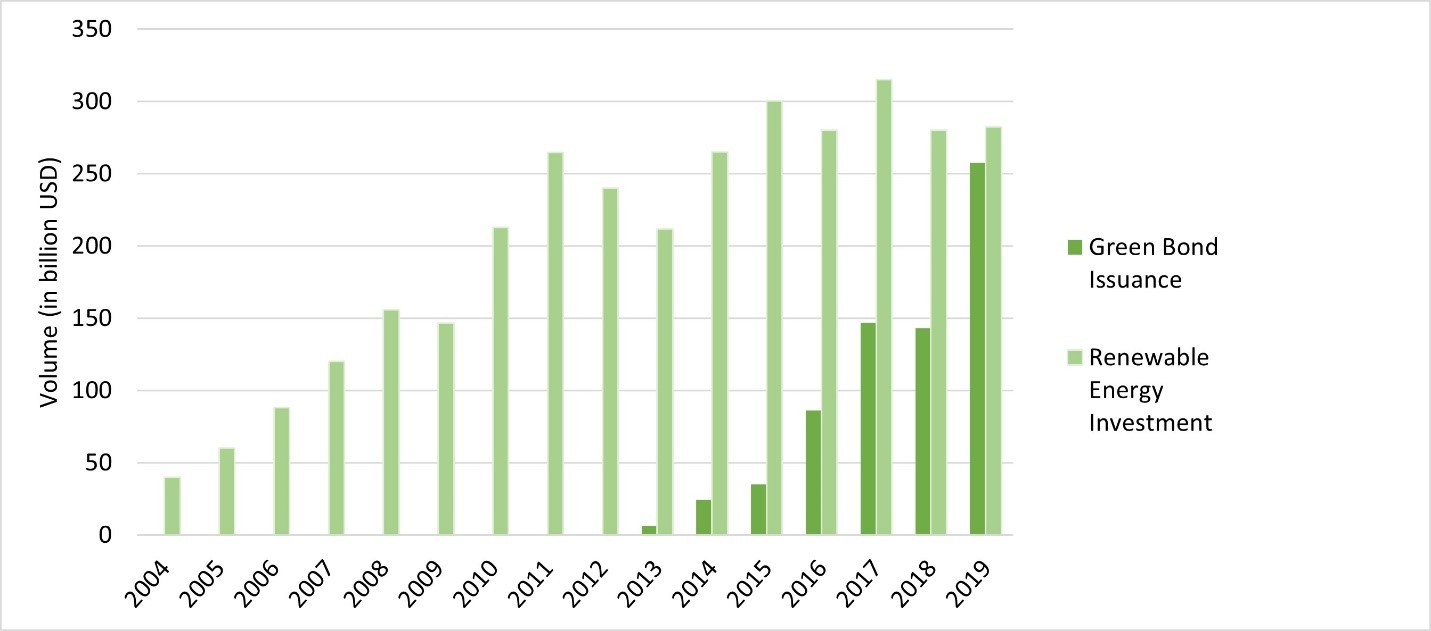

Figure 1. Global renewable energy investment and green bond issuance, 2004-2019

Source: Bloomberg and Bloomberg New Energy Finance.

THE GROWTH OF GREEN BONDS

New green bond issues reached over $250 billion globally in 2019, up from about $30 billion in 2014 and now on par with global renewable energy investment (Figure 1). The impressive increase in and diversification of green bonds since the first issuance by the World Bank in 2008 confirms the potential of this instrument to help finance the low-carbon transition. These assets are in high demand in many countries: Oversubscriptions, for example, were reported in 2020 for German as well as Egyptian green sovereign bonds and in 2019 for Chilean green bonds.

Green bonds help meet the financing requirements of the low-carbon transition but can also help accelerate the transition itself. In practice, green bonds can mobilize private capital and act as bridge financing at the project level to increase the availability of low-carbon technologies, filling the gap until carbon pricing initiatives can be sufficiently scaled up. One of the largest solar plants in the world, Noor-Ouarzazate Solar Power Station, leveraged more than $2.5 billion in financing, in part through green bonds. This project will substantially help Morocco reach its climate targets, increasing the share of renewable energy in its total energy mix to more than 40 percent with 2624 GWh of clean energy generation. By providing additional financing, green bonds can accelerate the mitigation process. This mobilization has been the most impressive in China, where the green bond market has grown to about $120 billion, quadrupling in size over four years.

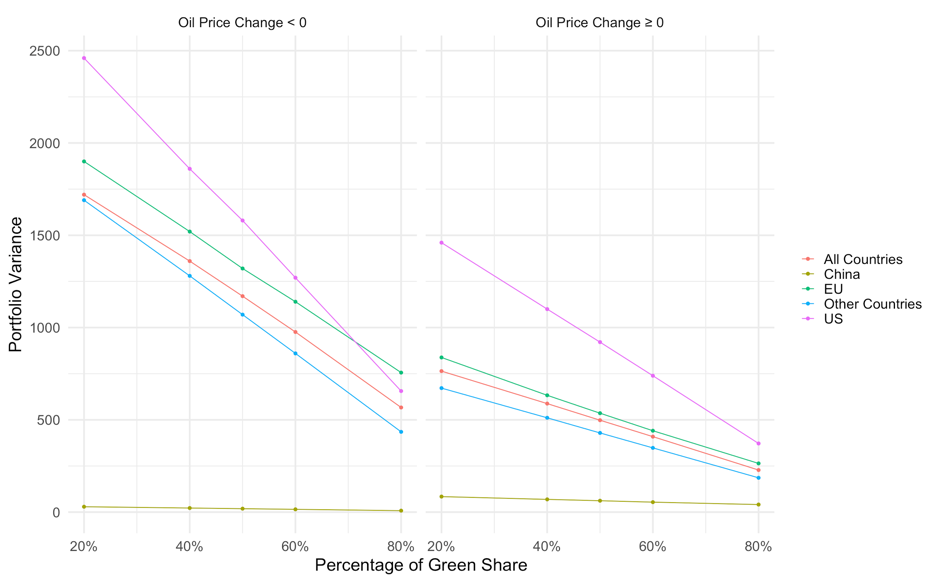

Green bonds also have several characteristics that make them attractive to financial market investors and issuers. In particular, green bonds can act as a stabilizing force on the financial market compared to conventional (e.g., fossil fuel) assets. The report presents initial evidence that issuing green bonds may have favorable effects on risk control for asset and portfolio holdings, as well as broaden and diversify the investor base. For example, Figure 2 shows that a larger share of green bonds leads to lower variance in portfolio returns during recessions (or negative oil price shocks), confirming their benefit as a hedging instrument, in particular in recessions or periods of declining fossil fuel prices.

Figure 2. Portfolio variance of different shares of green and fossil fuel bonds

Source: Author calculations based on S&P data.

But while Figure 1 shows that green bond issuance has increased together with renewable energy investment in recent decades, green bonds still represent a tiny share of financial market assets.

PRICE CARBON BETTER, AND ADD GREEN FINANCE

To accelerate the low carbon transition, carbon pricing has been widely proposed, with many researchers and policymakers supporting this approach. Carbon pricing supports a low carbon transition by making fossil fuel energy more expensive and subsidizing renewable energy production and use. In practice, carbon pricing has come in different forms such as an Emission Trading Scheme (ETS) and a carbon tax.

Financial market instruments have also been used to encourage the growth of renewable energy to achieve climate objectives. There has been an extensive flow of financial equity funds geared toward climate mitigation and adaptation policies, for example through alternative energy Exchange Traded Funds (ETFs). There is evidence that green assets have recently outperformed carbon-intensive assets (Figure 3). The report adds evidence confirming the benefits of issuing green bonds and investigates the combination of carbon taxes (e.g., a Pigouvian tax imposed on carbon-intensive goods and services) with green bonds (a market debt instrument to fund low-carbon investments).

Figure 3. Market performance of MSCI financial market indices

Source: MSCI.

There are three benefits of combining carbon tax and climate bonds to accelerate climate mitigation and adaptation efforts:

- Carbon pricing relies on substitution effects, but substitutes may not be currently available and need to be produced through private or private-public partnership investments. Green bonds can work as bridge finance for low carbon substitutes.

- Whereas carbon taxes can reduce negative externalities (and incentivize investments to reduce them), green bonds help to generate positive externality effects – both appear to be needed.

- Green bonds can bring about more financial stability when held as an asset class in portfolios and reduces the problem of “stranded assets.”

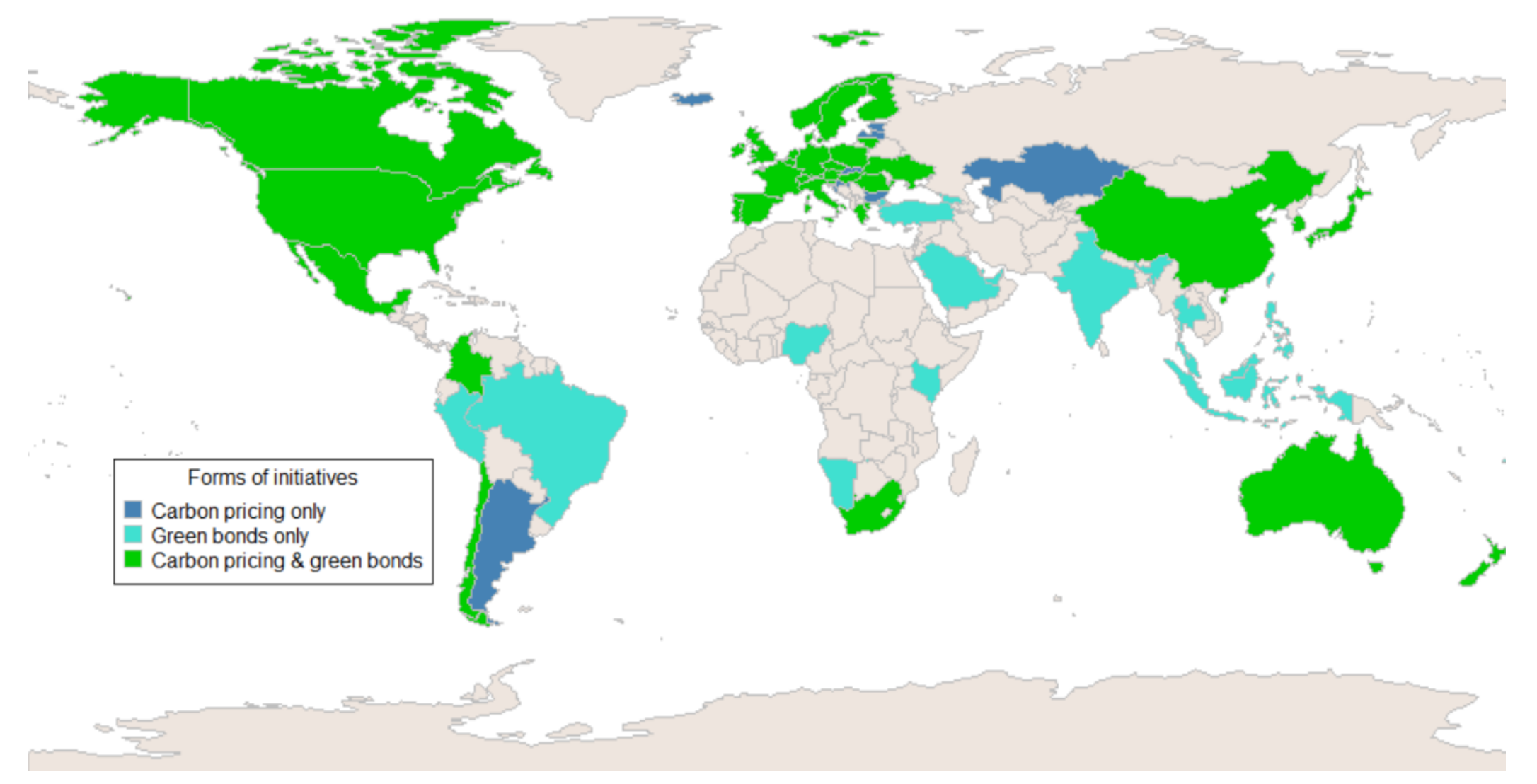

But in developing countries, carbon pricing and green bond initiatives are still in the initial stages (see Figure 4).

Figure 4. Countries with carbon pricing initiatives or green bonds

Source: Bloomberg Terminal data and World Bank Carbon Pricing Dashboard.

Note: Data for 2017-2020. Countries in green are those which have implemented both green bonds and carbon pricing at the federal or local level; countries in light blue have implemented green bonds only; countries in dark blue have implemented carbon pricing only.

The demand for green bonds is quickly rising in middle-income countries, but there are significant roadblocks for green investment even in advanced countries such as short-termism, small markets, liquidity, and governance problems. The report finds, however, that sustainable finance in the form of green bonds is on a steep learning curve and is potentially complementary to carbon pricing—in particular to carbon taxation.

THE MARKET IS STILL LEARNING

The green bond portion of the asset market is still small, market participants are heterogeneous, and people are still learning. Though green bond performance depends on many factors—such as the issuer, rating, currency, bond maturity, and sector—our report provides some encouraging messages:

- Green bonds appear to be less volatile than conventional bonds and assets, in particular those based on fossil-fired energy). Green bonds also appear to sell at a (negative) premium (see Kapraun and Scheins, 2019), while their Sharpe Ratio (the return-risk trade-off) is similar or even higher than that of conventional or fossil fuel-based bonds.

- The literature and our study suggest a strong co-movement between oil price fluctuations and carbon-intensive security returns. Green bonds exhibit lower volatility and little co-movement with fossil fuel-based asset prices and returns, and can therefore be a good hedge for investors.

Lower volatility and yields may provide private as well institutional investors with superior asset diversification opportunities and steady returns for the investors, as well as lower capital costs for issuers. Whereas with fossil fuel-backed assets, co-movement with oil price fluctuations makes carbon-dependent countries’ income vulnerable and increases financial volatility in certain sectors and countries.

Given the potential benefits of green fiscal instruments, governments should consider including them in their economic recovery plans. The combination of carbon taxes with green bonds allows long-run climate externalities to be addressed, and possibly even incentivizes the emergence of positive externalities. Though, during business cycle downturns a carbon tax levy might be less advisable while green bonds (and green assets in general) appear to be a useful portfolio and macroeconomic stabilizer.

This policy brief was originally shared on the Brookings Future Development blog.